| Multiple Linear Regression - Estimated Regression Equation |

| barrels_purchased[t] = -6894.98 -644.366unit_price[t] + 109889defl_price1[t] + 24133.2dum[t] + 597.488US_IND_PROD[t] -145145defl_price1dum[t] + 0.256361`barrels_purchased(t-1)`[t] + 0.248871`barrels_purchased(t-2)`[t] + 0.182822`barrels_purchased(t-3)`[t] + 0.208868`barrels_purchased(t-1s)`[t] + 3815.37M1[t] -186.403M2[t] -661.025M3[t] -714.16M4[t] -12688.4M5[t] -8040.19M6[t] -14738.3M7[t] -11691.4M8[t] -3075.78M9[t] -24301.5M10[t] -4841.88M11[t] -27.0577t + e[t] |

| Warning: you did not specify the column number of the endogenous series! The first column was selected by default. |

| Multiple Linear Regression - Ordinary Least Squares | |||||

| Variable | Parameter | S.D. | T-STAT H0: parameter = 0 | 2-tail p-value | 1-tail p-value |

| (Intercept) | -6895 | 1.104e+04 | -6.2450e-01 | 0.5326 | 0.2663 |

| unit_price | -644.4 | 397.2 | -1.6220e+00 | 0.1055 | 0.05277 |

| defl_price1 | +1.099e+05 | 7.703e+04 | +1.4270e+00 | 0.1545 | 0.07726 |

| dum | +2.413e+04 | 9150 | +2.6370e+00 | 0.008695 | 0.004348 |

| US_IND_PROD | +597.5 | 299.9 | +1.9920e+00 | 0.04703 | 0.02351 |

| defl_price1dum | -1.451e+05 | 4.531e+04 | -3.2040e+00 | 0.001471 | 0.0007354 |

| `barrels_purchased(t-1)` | +0.2564 | 0.04954 | +5.1750e+00 | 3.692e-07 | 1.846e-07 |

| `barrels_purchased(t-2)` | +0.2489 | 0.04876 | +5.1040e+00 | 5.246e-07 | 2.623e-07 |

| `barrels_purchased(t-3)` | +0.1828 | 0.04852 | +3.7680e+00 | 0.0001907 | 9.536e-05 |

| `barrels_purchased(t-1s)` | +0.2089 | 0.04098 | +5.0970e+00 | 5.431e-07 | 2.716e-07 |

| M1 | +3815 | 4390 | +8.6900e-01 | 0.3854 | 0.1927 |

| M2 | -186.4 | 4213 | -4.4240e-02 | 0.9647 | 0.4824 |

| M3 | -661 | 4218 | -1.5670e-01 | 0.8755 | 0.4378 |

| M4 | -714.2 | 4200 | -1.7000e-01 | 0.8651 | 0.4325 |

| M5 | -1.269e+04 | 4249 | -2.9860e+00 | 0.003004 | 0.001502 |

| M6 | -8040 | 4272 | -1.8820e+00 | 0.06061 | 0.03031 |

| M7 | -1.474e+04 | 4130 | -3.5690e+00 | 0.0004044 | 0.0002022 |

| M8 | -1.169e+04 | 4262 | -2.7430e+00 | 0.006378 | 0.003189 |

| M9 | -3076 | 4110 | -7.4830e-01 | 0.4547 | 0.2274 |

| M10 | -2.43e+04 | 4310 | -5.6380e+00 | 3.354e-08 | 1.677e-08 |

| M11 | -4842 | 4436 | -1.0920e+00 | 0.2757 | 0.1378 |

| t | -27.06 | 58.88 | -4.5950e-01 | 0.6461 | 0.3231 |

| Multiple Linear Regression - Regression Statistics | |

| Multiple R | 0.9739 |

| R-squared | 0.9484 |

| Adjusted R-squared | 0.9455 |

| F-TEST (value) | 334.2 |

| F-TEST (DF numerator) | 21 |

| F-TEST (DF denominator) | 382 |

| p-value | 0 |

| Multiple Linear Regression - Residual Statistics | |

| Residual Standard Deviation | 1.631e+04 |

| Sum Squared Residuals | 1.016e+11 |

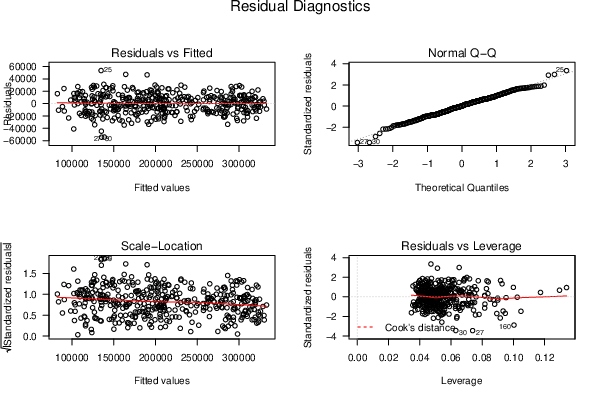

| Menu of Residual Diagnostics | |

| Description | Link |

| Histogram | Compute |

| Central Tendency | Compute |

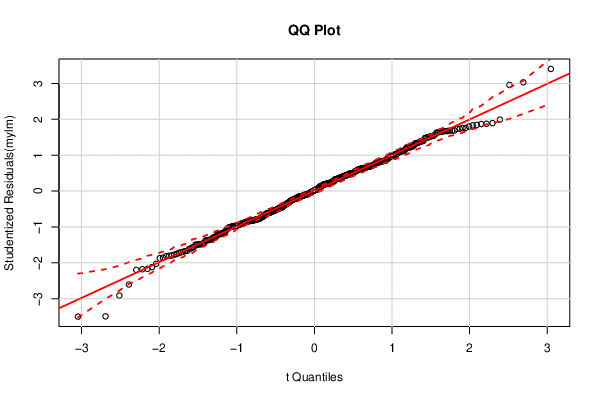

| QQ Plot | Compute |

| Kernel Density Plot | Compute |

| Skewness/Kurtosis Test | Compute |

| Skewness-Kurtosis Plot | Compute |

| Harrell-Davis Plot | Compute |

| Bootstrap Plot -- Central Tendency | Compute |

| Blocked Bootstrap Plot -- Central Tendency | Compute |

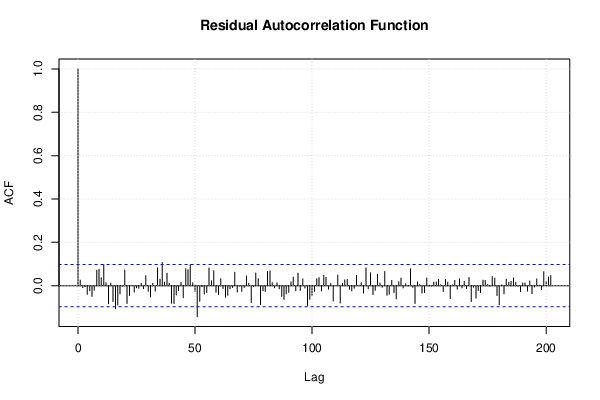

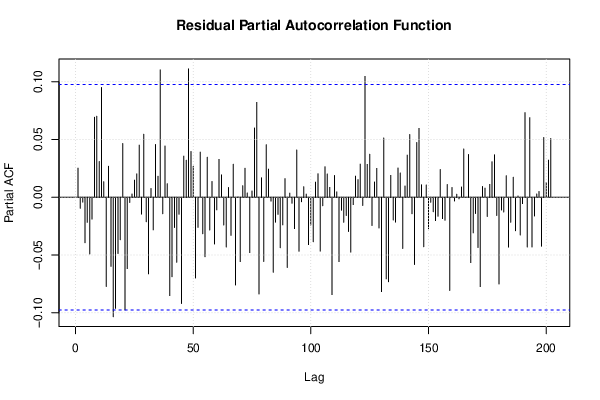

| (Partial) Autocorrelation Plot | Compute |

| Spectral Analysis | Compute |

| Tukey lambda PPCC Plot | Compute |

| Box-Cox Normality Plot | Compute |

| Summary Statistics | Compute |

| Ramsey RESET F-Test for powers (2 and 3) of fitted values |

> reset_test_fitted RESET test data: mylm RESET = 0.094702, df1 = 2, df2 = 380, p-value = 0.9097 |

| Ramsey RESET F-Test for powers (2 and 3) of regressors |

> reset_test_regressors RESET test data: mylm RESET = 0.61226, df1 = 42, df2 = 340, p-value = 0.973 |

| Ramsey RESET F-Test for powers (2 and 3) of principal components |

> reset_test_principal_components RESET test data: mylm RESET = 0.53392, df1 = 2, df2 = 380, p-value = 0.5867 |

| Variance Inflation Factors (Multicollinearity) |

> vif

unit_price defl_price1 dum

40.166900 69.313475 29.161236

US_IND_PROD defl_price1dum `barrels_purchased(t-1)`

49.312008 57.704473 18.159918

`barrels_purchased(t-2)` `barrels_purchased(t-3)` `barrels_purchased(t-1s)`

17.637154 17.495015 12.292517

M1 M2 M3

2.255756 2.077452 2.081585

M4 M5 M6

2.064527 2.112393 2.136109

M7 M8 M9

1.995894 2.126247 1.924205

M10 M11 t

2.116145 2.240650 71.598963

|