library(lattice)

library(lmtest)

library(car)

library(MASS)

n25 <- 25 #minimum number of obs. for Goldfeld-Quandt test

mywarning <- ''

par6 <- as.numeric(par6)

if(is.na(par6)) {

par6 <- 12

mywarning = 'Warning: you did not specify the seasonality. The seasonal period was set to s = 12.'

}

par1 <- as.numeric(par1)

if(is.na(par1)) {

par1 <- 1

mywarning = 'Warning: you did not specify the column number of the endogenous series! The first column was selected by default.'

}

if (par4=='') par4 <- 0

par4 <- as.numeric(par4)

if (!is.numeric(par4)) par4 <- 0

if (par5=='') par5 <- 0

par5 <- as.numeric(par5)

if (!is.numeric(par5)) par5 <- 0

x <- na.omit(t(y))

k <- length(x[1,])

n <- length(x[,1])

x1 <- cbind(x[,par1], x[,1:k!=par1])

mycolnames <- c(colnames(x)[par1], colnames(x)[1:k!=par1])

colnames(x1) <- mycolnames #colnames(x)[par1]

x <- x1

if (par3 == 'First Differences'){

(n <- n -1)

x2 <- array(0, dim=c(n,k), dimnames=list(1:n, paste('(1-B)',colnames(x),sep='')))

for (i in 1:n) {

for (j in 1:k) {

x2[i,j] <- x[i+1,j] - x[i,j]

}

}

x <- x2

}

if (par3 == 'Seasonal Differences (s)'){

(n <- n - par6)

x2 <- array(0, dim=c(n,k), dimnames=list(1:n, paste('(1-Bs)',colnames(x),sep='')))

for (i in 1:n) {

for (j in 1:k) {

x2[i,j] <- x[i+par6,j] - x[i,j]

}

}

x <- x2

}

if (par3 == 'First and Seasonal Differences (s)'){

(n <- n -1)

x2 <- array(0, dim=c(n,k), dimnames=list(1:n, paste('(1-B)',colnames(x),sep='')))

for (i in 1:n) {

for (j in 1:k) {

x2[i,j] <- x[i+1,j] - x[i,j]

}

}

x <- x2

(n <- n - par6)

x2 <- array(0, dim=c(n,k), dimnames=list(1:n, paste('(1-Bs)',colnames(x),sep='')))

for (i in 1:n) {

for (j in 1:k) {

x2[i,j] <- x[i+par6,j] - x[i,j]

}

}

x <- x2

}

if(par4 > 0) {

x2 <- array(0, dim=c(n-par4,par4), dimnames=list(1:(n-par4), paste(colnames(x)[par1],'(t-',1:par4,')',sep='')))

for (i in 1:(n-par4)) {

for (j in 1:par4) {

x2[i,j] <- x[i+par4-j,par1]

}

}

x <- cbind(x[(par4+1):n,], x2)

n <- n - par4

}

if(par5 > 0) {

x2 <- array(0, dim=c(n-par5*par6,par5), dimnames=list(1:(n-par5*par6), paste(colnames(x)[par1],'(t-',1:par5,'s)',sep='')))

for (i in 1:(n-par5*par6)) {

for (j in 1:par5) {

x2[i,j] <- x[i+par5*par6-j*par6,par1]

}

}

x <- cbind(x[(par5*par6+1):n,], x2)

n <- n - par5*par6

}

if (par2 == 'Include Seasonal Dummies'){

x2 <- array(0, dim=c(n,par6-1), dimnames=list(1:n, paste('M', seq(1:(par6-1)), sep ='')))

for (i in 1:(par6-1)){

x2[seq(i,n,par6),i] <- 1

}

x <- cbind(x, x2)

}

if (par2 == 'Include Monthly Dummies'){

x2 <- array(0, dim=c(n,11), dimnames=list(1:n, paste('M', seq(1:11), sep ='')))

for (i in 1:11){

x2[seq(i,n,12),i] <- 1

}

x <- cbind(x, x2)

}

if (par2 == 'Include Quarterly Dummies'){

x2 <- array(0, dim=c(n,3), dimnames=list(1:n, paste('Q', seq(1:3), sep ='')))

for (i in 1:3){

x2[seq(i,n,4),i] <- 1

}

x <- cbind(x, x2)

}

(k <- length(x[n,]))

if (par3 == 'Linear Trend'){

x <- cbind(x, c(1:n))

colnames(x)[k+1] <- 't'

}

print(x)

(k <- length(x[n,]))

head(x)

df <- as.data.frame(x)

(mylm <- lm(df))

(mysum <- summary(mylm))

if (n > n25) {

kp3 <- k + 3

nmkm3 <- n - k - 3

gqarr <- array(NA, dim=c(nmkm3-kp3+1,3))

numgqtests <- 0

numsignificant1 <- 0

numsignificant5 <- 0

numsignificant10 <- 0

for (mypoint in kp3:nmkm3) {

j <- 0

numgqtests <- numgqtests + 1

for (myalt in c('greater', 'two.sided', 'less')) {

j <- j + 1

gqarr[mypoint-kp3+1,j] <- gqtest(mylm, point=mypoint, alternative=myalt)$p.value

}

if (gqarr[mypoint-kp3+1,2] < 0.01) numsignificant1 <- numsignificant1 + 1

if (gqarr[mypoint-kp3+1,2] < 0.05) numsignificant5 <- numsignificant5 + 1

if (gqarr[mypoint-kp3+1,2] < 0.10) numsignificant10 <- numsignificant10 + 1

}

gqarr

}

bitmap(file='test0.png')

plot(x[,1], type='l', main='Actuals and Interpolation', ylab='value of Actuals and Interpolation (dots)', xlab='time or index')

points(x[,1]-mysum$resid)

grid()

dev.off()

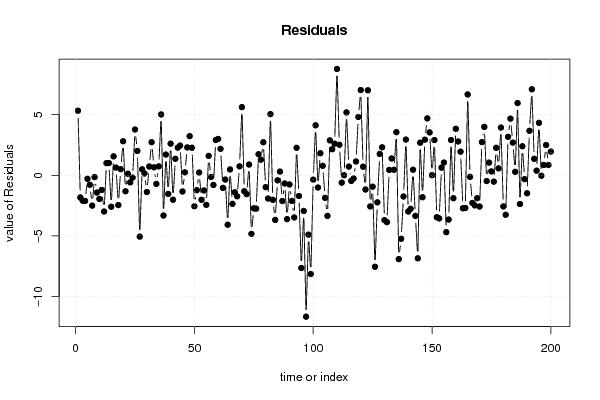

bitmap(file='test1.png')

plot(mysum$resid, type='b', pch=19, main='Residuals', ylab='value of Residuals', xlab='time or index')

grid()

dev.off()

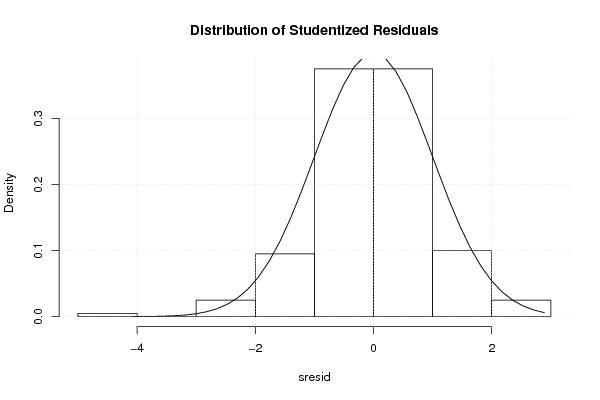

bitmap(file='test2.png')

sresid <- studres(mylm)

hist(sresid, freq=FALSE, main='Distribution of Studentized Residuals')

xfit<-seq(min(sresid),max(sresid),length=40)

yfit<-dnorm(xfit)

lines(xfit, yfit)

grid()

dev.off()

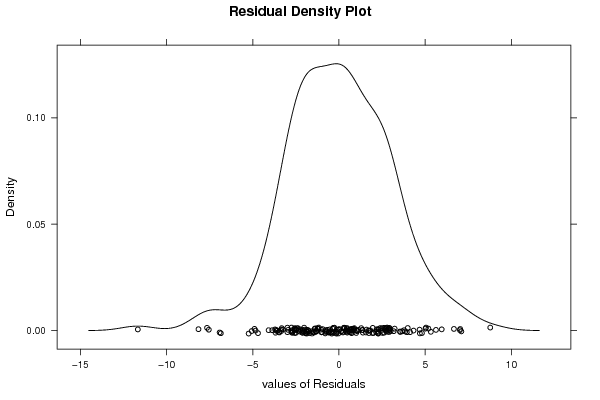

bitmap(file='test3.png')

densityplot(~mysum$resid,col='black',main='Residual Density Plot', xlab='values of Residuals')

dev.off()

bitmap(file='test4.png')

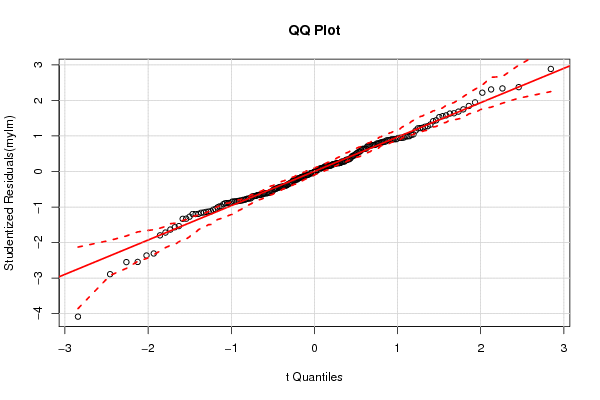

qqPlot(mylm, main='QQ Plot')

grid()

dev.off()

(myerror <- as.ts(mysum$resid))

bitmap(file='test5.png')

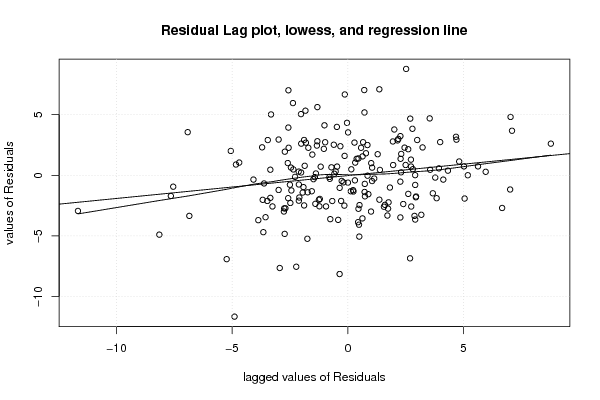

dum <- cbind(lag(myerror,k=1),myerror)

dum

dum1 <- dum[2:length(myerror),]

dum1

z <- as.data.frame(dum1)

print(z)

plot(z,main=paste('Residual Lag plot, lowess, and regression line'), ylab='values of Residuals', xlab='lagged values of Residuals')

lines(lowess(z))

abline(lm(z))

grid()

dev.off()

bitmap(file='test6.png')

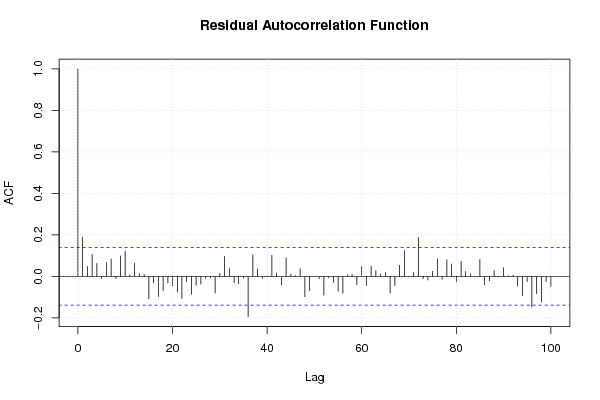

acf(mysum$resid, lag.max=length(mysum$resid)/2, main='Residual Autocorrelation Function')

grid()

dev.off()

bitmap(file='test7.png')

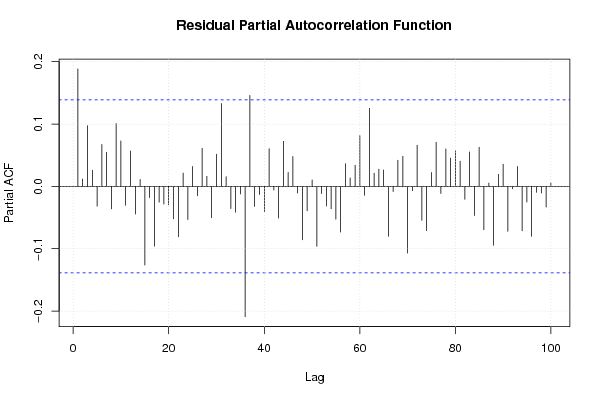

pacf(mysum$resid, lag.max=length(mysum$resid)/2, main='Residual Partial Autocorrelation Function')

grid()

dev.off()

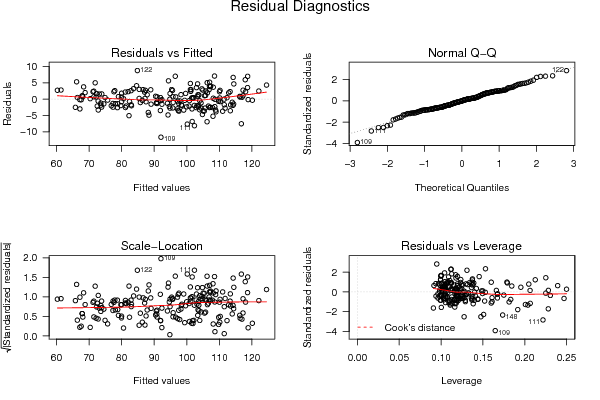

bitmap(file='test8.png')

opar <- par(mfrow = c(2,2), oma = c(0, 0, 1.1, 0))

plot(mylm, las = 1, sub='Residual Diagnostics')

par(opar)

dev.off()

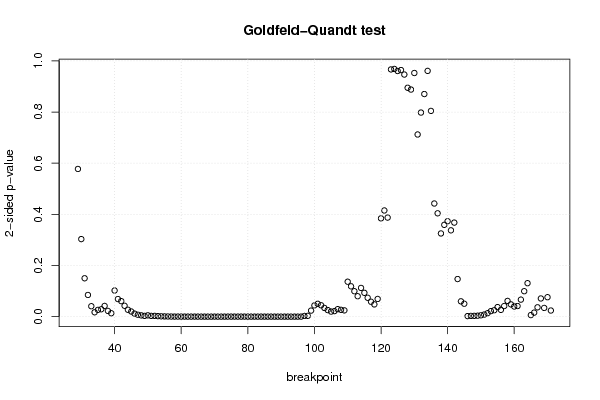

if (n > n25) {

bitmap(file='test9.png')

plot(kp3:nmkm3,gqarr[,2], main='Goldfeld-Quandt test',ylab='2-sided p-value',xlab='breakpoint')

grid()

dev.off()

}

load(file='createtable')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a, 'Multiple Linear Regression - Estimated Regression Equation', 1, TRUE)

a<-table.row.end(a)

myeq <- colnames(x)[1]

myeq <- paste(myeq, '[t] = ', sep='')

for (i in 1:k){

if (mysum$coefficients[i,1] > 0) myeq <- paste(myeq, '+', '')

myeq <- paste(myeq, signif(mysum$coefficients[i,1],6), sep=' ')

if (rownames(mysum$coefficients)[i] != '(Intercept)') {

myeq <- paste(myeq, rownames(mysum$coefficients)[i], sep='')

if (rownames(mysum$coefficients)[i] != 't') myeq <- paste(myeq, '[t]', sep='')

}

}

myeq <- paste(myeq, ' + e[t]')

a<-table.row.start(a)

a<-table.element(a, myeq)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a, mywarning)

a<-table.row.end(a)

a<-table.end(a)

table.save(a,file='mytable1.tab')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Multiple Linear Regression - Ordinary Least Squares', 6, TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'Variable',header=TRUE)

a<-table.element(a,'Parameter',header=TRUE)

a<-table.element(a,'S.D.',header=TRUE)

a<-table.element(a,'T-STAT

H0: parameter = 0',header=TRUE)

a<-table.element(a,'2-tail p-value',header=TRUE)

a<-table.element(a,'1-tail p-value',header=TRUE)

a<-table.row.end(a)

for (i in 1:k){

a<-table.row.start(a)

a<-table.element(a,rownames(mysum$coefficients)[i],header=TRUE)

a<-table.element(a,formatC(signif(mysum$coefficients[i,1],5),format='g',flag='+'))

a<-table.element(a,formatC(signif(mysum$coefficients[i,2],5),format='g',flag=' '))

a<-table.element(a,formatC(signif(mysum$coefficients[i,3],4),format='e',flag='+'))

a<-table.element(a,formatC(signif(mysum$coefficients[i,4],4),format='g',flag=' '))

a<-table.element(a,formatC(signif(mysum$coefficients[i,4]/2,4),format='g',flag=' '))

a<-table.row.end(a)

}

a<-table.end(a)

table.save(a,file='mytable2.tab')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a, 'Multiple Linear Regression - Regression Statistics', 2, TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a, 'Multiple R',1,TRUE)

a<-table.element(a,formatC(signif(sqrt(mysum$r.squared),6),format='g',flag=' '))

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a, 'R-squared',1,TRUE)

a<-table.element(a,formatC(signif(mysum$r.squared,6),format='g',flag=' '))

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a, 'Adjusted R-squared',1,TRUE)

a<-table.element(a,formatC(signif(mysum$adj.r.squared,6),format='g',flag=' '))

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a, 'F-TEST (value)',1,TRUE)

a<-table.element(a,formatC(signif(mysum$fstatistic[1],6),format='g',flag=' '))

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a, 'F-TEST (DF numerator)',1,TRUE)

a<-table.element(a, signif(mysum$fstatistic[2],6))

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a, 'F-TEST (DF denominator)',1,TRUE)

a<-table.element(a, signif(mysum$fstatistic[3],6))

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a, 'p-value',1,TRUE)

a<-table.element(a,formatC(signif(1-pf(mysum$fstatistic[1],mysum$fstatistic[2],mysum$fstatistic[3]),6),format='g',flag=' '))

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a, 'Multiple Linear Regression - Residual Statistics', 2, TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a, 'Residual Standard Deviation',1,TRUE)

a<-table.element(a,formatC(signif(mysum$sigma,6),format='g',flag=' '))

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a, 'Sum Squared Residuals',1,TRUE)

a<-table.element(a,formatC(signif(sum(myerror*myerror),6),format='g',flag=' '))

a<-table.row.end(a)

a<-table.end(a)

table.save(a,file='mytable3.tab')

myr <- as.numeric(mysum$resid)

myr

a <-table.start()

a <- table.row.start(a)

a <- table.element(a,'Menu of Residual Diagnostics',2,TRUE)

a <- table.row.end(a)

a <- table.row.start(a)

a <- table.element(a,'Description',1,TRUE)

a <- table.element(a,'Link',1,TRUE)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'Histogram',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_histogram.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'Central Tendency',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_centraltendency.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'QQ Plot',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_fitdistrnorm.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'Kernel Density Plot',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_density.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'Skewness/Kurtosis Test',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_skewness_kurtosis.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'Skewness-Kurtosis Plot',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_skewness_kurtosis_plot.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'Harrell-Davis Plot',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_harrell_davis.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'Bootstrap Plot -- Central Tendency',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_bootstrapplot1.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'Blocked Bootstrap Plot -- Central Tendency',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_bootstrapplot.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'(Partial) Autocorrelation Plot',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_autocorrelation.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'Spectral Analysis',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_spectrum.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'Tukey lambda PPCC Plot',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_tukeylambda.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <-table.element(a,'Box-Cox Normality Plot',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_boxcoxnorm.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a <- table.row.start(a)

a <- table.element(a,'Summary Statistics',1,header=TRUE)

a <- table.element(a,hyperlink( paste('https://supernova.wessa.net/rwasp_summary1.wasp?convertgetintopost=1&data=',paste(as.character(mysum$resid),sep='',collapse=' '),sep='') ,'Compute','Click here to examine the Residuals.'),1)

a <- table.row.end(a)

a<-table.end(a)

table.save(a,file='mytable7.tab')

if(n < 200) {

a<-table.start()

a<-table.row.start(a)

a<-table.element(a, 'Multiple Linear Regression - Actuals, Interpolation, and Residuals', 4, TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a, 'Time or Index', 1, TRUE)

a<-table.element(a, 'Actuals', 1, TRUE)

a<-table.element(a, 'Interpolation

Forecast', 1, TRUE)

a<-table.element(a, 'Residuals

Prediction Error', 1, TRUE)

a<-table.row.end(a)

for (i in 1:n) {

a<-table.row.start(a)

a<-table.element(a,i, 1, TRUE)

a<-table.element(a,formatC(signif(x[i],6),format='g',flag=' '))

a<-table.element(a,formatC(signif(x[i]-mysum$resid[i],6),format='g',flag=' '))

a<-table.element(a,formatC(signif(mysum$resid[i],6),format='g',flag=' '))

a<-table.row.end(a)

}

a<-table.end(a)

table.save(a,file='mytable4.tab')

if (n > n25) {

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Goldfeld-Quandt test for Heteroskedasticity',4,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'p-values',header=TRUE)

a<-table.element(a,'Alternative Hypothesis',3,header=TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'breakpoint index',header=TRUE)

a<-table.element(a,'greater',header=TRUE)

a<-table.element(a,'2-sided',header=TRUE)

a<-table.element(a,'less',header=TRUE)

a<-table.row.end(a)

for (mypoint in kp3:nmkm3) {

a<-table.row.start(a)

a<-table.element(a,mypoint,header=TRUE)

a<-table.element(a,formatC(signif(gqarr[mypoint-kp3+1,1],6),format='g',flag=' '))

a<-table.element(a,formatC(signif(gqarr[mypoint-kp3+1,2],6),format='g',flag=' '))

a<-table.element(a,formatC(signif(gqarr[mypoint-kp3+1,3],6),format='g',flag=' '))

a<-table.row.end(a)

}

a<-table.end(a)

table.save(a,file='mytable5.tab')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Meta Analysis of Goldfeld-Quandt test for Heteroskedasticity',4,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'Description',header=TRUE)

a<-table.element(a,'# significant tests',header=TRUE)

a<-table.element(a,'% significant tests',header=TRUE)

a<-table.element(a,'OK/NOK',header=TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'1% type I error level',header=TRUE)

a<-table.element(a,signif(numsignificant1,6))

a<-table.element(a,formatC(signif(numsignificant1/numgqtests,6),format='g',flag=' '))

if (numsignificant1/numgqtests < 0.01) dum <- 'OK' else dum <- 'NOK'

a<-table.element(a,dum)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'5% type I error level',header=TRUE)

a<-table.element(a,signif(numsignificant5,6))

a<-table.element(a,signif(numsignificant5/numgqtests,6))

if (numsignificant5/numgqtests < 0.05) dum <- 'OK' else dum <- 'NOK'

a<-table.element(a,dum)

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'10% type I error level',header=TRUE)

a<-table.element(a,signif(numsignificant10,6))

a<-table.element(a,signif(numsignificant10/numgqtests,6))

if (numsignificant10/numgqtests < 0.1) dum <- 'OK' else dum <- 'NOK'

a<-table.element(a,dum)

a<-table.row.end(a)

a<-table.end(a)

table.save(a,file='mytable6.tab')

}

}

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Ramsey RESET F-Test for powers (2 and 3) of fitted values',1,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

reset_test_fitted <- resettest(mylm,power=2:3,type='fitted')

a<-table.element(a,paste('',RC.texteval('reset_test_fitted'),'',sep=''))

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'Ramsey RESET F-Test for powers (2 and 3) of regressors',1,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

reset_test_regressors <- resettest(mylm,power=2:3,type='regressor')

a<-table.element(a,paste('',RC.texteval('reset_test_regressors'),'',sep=''))

a<-table.row.end(a)

a<-table.row.start(a)

a<-table.element(a,'Ramsey RESET F-Test for powers (2 and 3) of principal components',1,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

reset_test_principal_components <- resettest(mylm,power=2:3,type='princomp')

a<-table.element(a,paste('',RC.texteval('reset_test_principal_components'),'',sep=''))

a<-table.row.end(a)

a<-table.end(a)

table.save(a,file='mytable8.tab')

a<-table.start()

a<-table.row.start(a)

a<-table.element(a,'Variance Inflation Factors (Multicollinearity)',1,TRUE)

a<-table.row.end(a)

a<-table.row.start(a)

vif <- vif(mylm)

a<-table.element(a,paste('',RC.texteval('vif'),'',sep=''))

a<-table.row.end(a)

a<-table.end(a)

table.save(a,file='mytable9.tab')

|